The multifamily market is at a crossroads. While demand remains robust, a surge in new supply is creating headwinds, impacting rent growth and occupancy. As we move into 2025, understanding these dynamics is crucial for investors and operators. This article breaks down the key trends and offers insights for navigating the evolving landscape.

Demand Meets Supply: A Balancing Act

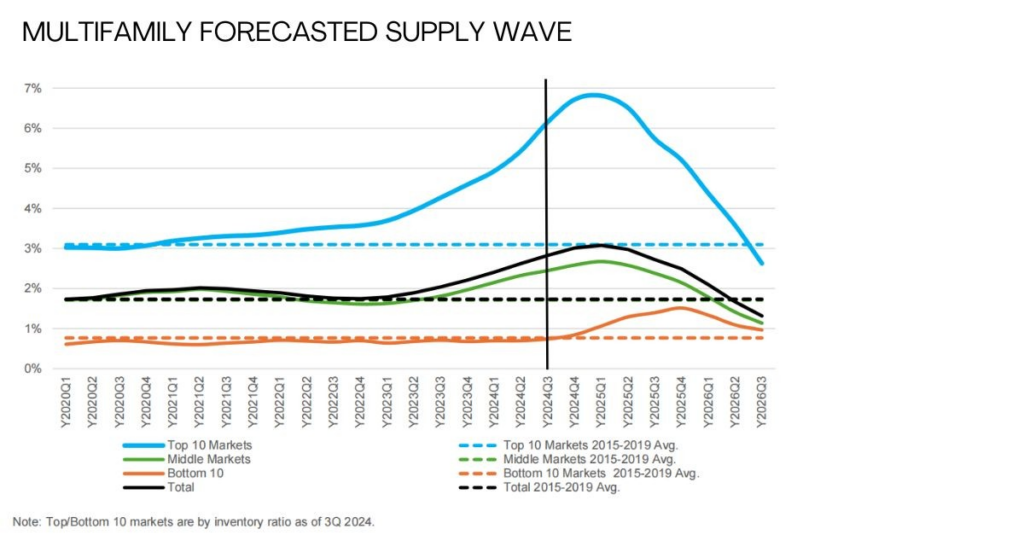

Demand for multifamily housing has shown remarkable resilience, with nearly 490,000 units absorbed through the third quarter of 2024. However, this strong demand is being tested by an even greater wave of new supply, totaling approximately 560,000 units. This imbalance has led to subdued rent growth and pressure on occupancy rates. The sheer volume of new units hitting the market has tipped the scales, creating a more competitive environment.

The Supply Peak and Beyond:

The peak of this new supply wave is expected to hit in mid-2025. This influx will likely continue to exert downward pressure on rents and occupancy in the short term. However, there’s a light at the end of the tunnel. By the end of 2025 and into 2026, the pace of new deliveries is projected to decrease. This could provide an opportunity for market fundamentals to recover, potentially leading to improved rent growth and occupancy. Current forecasts suggest rent growth of 2.2% and a modest increase in vacancies to 6.2% by the end of 2025.

Regional Disparities: Where Supply Matters Most:

The distribution of new supply isn’t uniform across the country. The Sun Belt and Mountain West regions are experiencing the largest increases, with some markets anticipating over 5% growth in inventory in 2025. Conversely, major gateway metros and smaller tertiary markets are seeing much lower levels of new supply, averaging around 0.7%. This disparity is creating a two-tiered market. Areas with limited new construction are expected to outperform, often appearing among the top markets for projected gross income growth. Conversely, regions grappling with high supply are likely to see continued pressure on rent growth, potentially landing them on the list of underperforming markets.

The Debt Market: A Volatile Landscape:

The debt market has shown signs of improvement in 2024, but volatility remains a concern. While the 10-year Treasury rate compressed in the third quarter and cap rates stabilized somewhat, the rate remains elevated and subject to fluctuations. This volatility continues to impact valuations, with cap rates up 30 basis points year-over-year and cap rate spreads remaining tight. Consequently, property prices have continued to decline, although the rate of decline has slowed.

Looking Ahead: Cautious Optimism:

Despite the challenges, the multifamily market is expected to gain momentum in 2025 and 2026 as the peak of new supply passes and interest rate volatility subsides. Origination activity is projected to increase, assuming rate stabilization and the avoidance of an economic downturn. While performance may not immediately reach long-run averages, the multifamily sector has demonstrated resilience and a capacity for stable growth.

Key Takeaways for Investors:

- Monitor Supply: Closely track new supply in your target markets. Understanding the local supply dynamics is crucial for making informed investment decisions.

- Conservative Underwriting: Given the current uncertainties, conservative underwriting is paramount. Factor in potential rent pressures and vacancy fluctuations.

- Focus on Fundamentals: Prioritize markets with strong underlying fundamentals, such as job growth and population increases.

- Stay Informed: Keep abreast of market trends, interest rate movements, and economic indicators.

The 2025 multifamily market presents both challenges and opportunities. By understanding the interplay of supply, demand, and financial conditions, investors can position themselves for success in this dynamic environment.